China Manufacturing PMI (Aug) M/M 49.2 vs. Exp. 50.0 (Prev. 50.1)

China Non-Manufacturing PMI (Aug) M/M 56.3 (Prev. 55.6)

China HSBC Manufacturing PMI (Aug) M/M 47.6 (Prev. 49.3)

The ECB is said to have no preferred option for the bond purchase plan yet, and is said to plan to give central bank governors the bond proposals on September 4th, and then 24 hours to digest the bond plan.

Spain’s PM Rajoy says Spain will consider seeking extra aid from Europe on top of a EUR 100bln rescue of its financial sector but does not see any need for any new conditions. He added that he wanted to see details of the ECB’s bond buying programme before deciding whether to proceed with a request.

German finance minister Schaeuble has said it is unlikely that we will see ECB supervision laws this year, adding that the central bank would not have the capacity to oversee all European banks, with supervision of the 'big' banks more likely.

UK Lloyds Business Barometer (Aug) M/M 10 (Prev. -8)

The OECD is expected to downgrade its forecasts for Britain when it releases its interim economic assessments for G7 economies on Thursday. In May, the group predicted Britain would grow 0.5% in 2012 and 1.9% next year. Independent forecasters now expect the economy to shrink by about 0.2% this year.

EDIT:

EUROPE: The appetite for yield is seeing some funds move back into shorter-dated Italian and Spanish bonds, the WSJ reports, as expectations grow of ECB action.

Wtorek

- RBA podejmuje decyzję o stopach procentowych

- GDP szwajcarii, pytanie jak to się odbije na kursie eurchf i eur usd

- ISM w USA (wskaźnik idealnie pod dual mandate Fed'u )

- PPI w EZ

Środa

- GDP Australii i paczka danych z Chin, coś dla miłośników kangurów. - Bank Kanady podejmuje decyzję o stopach procentowych

Czwartek

- zatrudnienie w Australii (znowu te kangury ) - szef BoJ przemawia

- BoE decyzja o QE

- BoE decyzja o stopach

- ECB decyzja o stopach, ostry dzień, oni z BoE to się chyba jakoś umawiają

Piątek

- inflacja UK

- zatrudnienie w Kanadzie

- NFP w USA

- bezrobocie w USA

EUROZONE: Timeline of key events in the eurozone for next few sessions:

- Sep 3 ECB Draghi to meet EU Rehn/Barnier behind closed doors

- Sep 3 Spain regional Q2 public finance - Sep 3 European final manufacturing PMI data

- Sep 4 Italy Monti to meet France Hollande

- Sep 4 EU Van Rompuy to meet Germany Merkel in Berlin

- Sep 4 EFSF sells new 3-month Bills for up to E2.0bln

- Sep 4 Greece to sell 26-week T-bills for E875mln

- Sep 5 EU Van Rompuy to meet France Hollande in Paris

- Sep 5/6 Euro-Working Group/Economic Finance Committee meetings

- Sep 6 OECD Economic Outlook report

- Sep 6 ECB meeting, Draghi to give ECB Staff Forecasts - Sep 6 German Merkel to visit Spain PM Rajoy - Sep 6 EU Barroso to meet Italy PM Monti - Sep 6 Spain taps 4.25% 2016-/4.00% 2015-/3.40% 2014 Bono bonds - Sep 6 Eurozone Q2 GDP data (2nd estimate)

Strong week for precious metals while iron ore plummeted

03-wrz-2012

Commodity markets finished a strong month of August with an added boost given by Chairman Bernanke last Friday. In a long awaited speech, he left the market with the impression that additional stimulus could be implemented to spark economic growth and employment.

Before the next Federal Open Market Committee meeting on September 12-13, at which time such measures might be announced, we will keenly watch the monthly US employment report on Friday. Another strong reading like last month could sway the FOMC towards doing nothing, particularly if the FOMC considers the adverse impact that easing might have on an asset class like commodities, where food and energy prices are trading close to yearly highs at a time of weak global activity.

The DJ-UBS commodity index rose 0.5 percent over the week and returned 1.3 percent during August. The positive return was driven by precious metals, especially silver and gold, which both broke higher. The energy sector came second, following a bounce in natural gas, while both Brent and WTI crude have settled into ranges following a strong rally during the early parts of August. Industrial metals suffered losses as Chinese economic data continues to weaken, with iron ore in particular taking the brunt, falling another 10 percent last week after having dropped by almost one quarter during August. A small agriculture sector gain was driven by cocoa and livestock, as recent strong momentum in corn has begun to slow.

Hedge Funds joining the gold rally

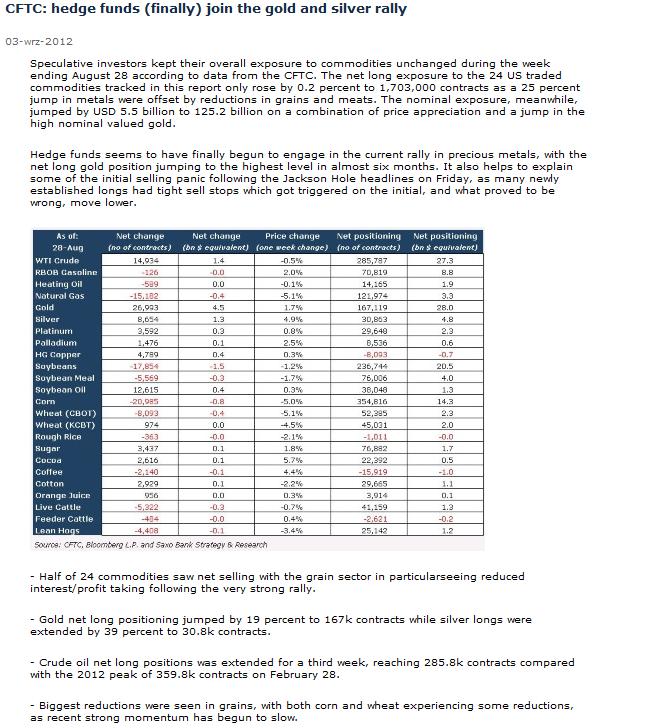

Investors in gold exchange traded products have continued to increase their exposure to gold and silver both before and after the recent move higher. Gold ETPs added 364k ounces during the last week of August to a new record of 79.1 million ounces (moz). This took the monthly inflow to 2.07 moz and 3.32 moz over the year, according to data compiled by Bloomberg. While these investors have been busy pulling their wallets out, hedge funds and other large investors have been much more reluctant, as lack of momentum and a month-long period of range trading has reduced interest.

That was until recently, when this leveraged investor segment finally jumped back to life, reacting to the rise in prices. During the two week period ending August 28, leveraged investors increased their net long exposure through futures and options by almost 5 moz, according to the CFTC. This was the biggest jump since July 2011 and it has brought their net long position up to 16.7 moz, still below the 2012 peak of 22.2 moz and the all-time high of 28.9 moz recorded one year ago. Silver has been even more impressive, with speculative long positions through futures more than doubling during the same two-week period.

The speech by Chairman Bernanke on Friday initially triggered a small sell-off, as no concrete new measures were announced. But the fact that the market quickly found support below 1,650 ahead of the 200 day moving average, and subsequently rallied by more than 40 dollars, indicates to me that many, regardless of the outcome, stood ready to pick up the yellow metal if lower prices emerged.

Gold now probably needs some time to consolidate, especially ahead of the European Central Bank meeting this Thursday and the very important monthly job report from the US on Friday. Main support still lies below 1,630, the top of the previous range, and the 200 day moving average at 1,642 while. Initial resistance will be offered ahead of 1,700 followed by the March 12 high at 1,717.

Iron ore the big loser in August

The price of iron ore, one of the two main components in the production of steel, dropped by almost one quarter during August thereby bringing the year to date loss to more than one-third. Slowing demand for steel in China, the world's largest consumer, combined with already high volumes of stock in Chinese ports looking for a home have done most of the damage to prices. Being such a key component in global manufacturing it highlights the weakness in this area and the market will be looking out for some additional Chinese stimulus to help clear inventories and bring support to the price. Until that happens the price, currently trading at an almost three year low at 89 dollars per tonne is likely to remain below USD 100 per tonne.

Crude oil range-bound as supply side issues lend support

Brent crude oil is currently stuck between 111.50 and 116.50 as supply side worries and geo-politics continue to lend support despite bearish fundamentals of weak demand and adequate supplies. Manufacturing activity in China is contracting faster than expected while hurricane Isaac caused no major damage to the supply system and following a brief period of WTI crude outperformance the discount to Brent crude widened again to the current level above 18 dollars as production resumed.

The stand-off between Iran and Western countries over its nuclear attention will not go away especially not after the International Atomic Energy Agency's (IAEA) estimates that Iran has now doubled production capacity at its main nuclear site. While Iran continues to deny that the use is for military purposes the patience among Israeli politicians is wearing thin as the window of opportunity for an attack is slowly closing. Whether an attack will cause a major spike in oil prices mostly depends on what response it will trigger from Iran but until the situation changes, spike or not, a risk premium is being priced in at current levels.

The US government is also getting trigger happy but more in terms of triggering the Strategic Petroleum Reserve button. The relentless rise in gasoline prices which now for the third time in little over a year is approaching the physiological level of USD 4 per gallon has raised concerns about the impact on US consumers and the Presidential election campaign which is now underway. The other major members of the International Energy Agency (IEA) and the organisation itself have so far been very reluctant in joining this call, primarily from running the risk that it could be seen as being politically motivated and therefore have limited impact. The last release during the Libyan war in 2012 did not manage to get the lasting impact which was hoped for and the IEA would not want to be seen as not being able to successfully manage such a release. The US accounts for almost half of all SPR.

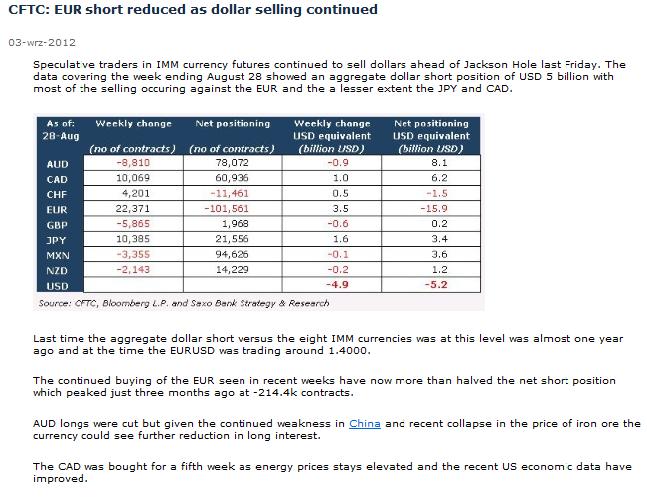

For the coming week the attention will turn to the ECB meeting on Thursday and the US unemployment report on Friday in order to see whether additional (supporting) monetary stimulus is forthcoming. The weaker dollar in recent weeks has also supported the energy sector but with recent data pointing towards speculative investors now being net short of dollars for the first time in almost one year, any worsening situation could drive investors back into the dollar and out of commodities.

Speculative positioning as of August 28 was almost unchanged at 108 million barrels in Brent crude while money managers increased their net long position in WTI crude by 8 percent to a four month high at 190 million barrels.

Grain markets take stock

Slowing upside momentum in corn and wheat triggered some profit taking in the two grains last week while soybeans continued to see new record highs. Soybeans are driven by continued strong export numbers with demand rationing still not evident. Wheat lost some of its recent support as the Russian government's food security commission announced that, despite a sharp reduction in output following a summer of drought, there were no plans to limit exports. Overall high prices in all three grains will be necessary to protect diminishing global stock levels. Corn is probably the one most exposed to profit taking given the size of the speculative long position. Any correction however below USD 7.82 should probably find new buyers thereby cushioning and halting the fall fairly quickly.

Nie masz wymaganych uprawnień, aby zobaczyć pliki załączone do tego posta.

... zbieraj pips do pipa bo jak nie to z depo będzie lipa... G."niemiaszek"

Czas wracać do normalnej pracy... Poniedziałek był takim małym przedłużeniem wakacji, teraz zaczyna się nieco poważniej. Dzięki Stforex za kalendarz, zaczynamy od RBA, na szczeście ktoś już to opisał więc nie muszę sam wymyślać:

Not Much Excitement For RBA Decision But Risks Present

By Adam Button || September 3, 2012 at 19:05 GMT

The highlight of Asia-Pacific trading will be the RBA decision at 0430 GMT.

All 24 economists surveyed by Bloomberg expect no change from the 3.50% cash target. Economists expect the RBA to hold rates again in October and then cut at the November meeting.

The OIS market is showing a 20% chance of a cut today and is fully priced for two cuts before the end of the year.

If the RBA takes a strongly dovish stance, we could see AUD/USD back to parity in short order.

Comments about China will be interesting, The most-recent statement said “China’s growth has moderated to a more sustainable pace, but does not appear to be slowing further.”

Herald Sun RBA watcher McCrann believes the RBA will decide what to do next once the direction of the economies in Europe, the US and China are more clear.

Inaczej mówiąc największe ryzyko jest w zaskakującej zmianie stóp której szanse wydają się być na poziomie 20%. Ryzyko jest w dół czyli jak będzie zmiana to tylko cięcie stóp i zjazd o 250 pip.

Natomiast w przypadku pozostania stóp na nie zmienionym poziomie, to czy A$ będzie dalej się zsuwał czy nie będzie zależało od tego jak RBA widzi najbliższą przyszłość, szczególnie w obliczu spadających cen rudy żelaza oraz zamówień z Chin. A w zasadzie w ogóle sytuacji w Chinach bo dolar Australijski stał się proxy juana (w nieco luźniejszym pojęciu proxy)

Jakże często ludzie mają już gotową opinię zanim zdążą pojąć istotę rzeczy.

A gdy już ta istota w pełni do nich dotrze, jakże często muszą zmagać się z konsekwencjami swojej opinii ;-)

AUSTRALIA: The RBA keeps the official cash rate unchanged at 3.50%, as expected.

AUSTRALIA: From The RBA: "At today's meeting, the Board judged that, with inflation expected to be consistent with the target and growth close to trend, but with a more subdued international outlook than was the case a few months ago, the stance of monetary policy remained appropriate."

AUSTRALIA: From The RBA: "As a result of the sequence of earlier decisions, interest rates for borrowers are a little below their medium-term averages. The impact of those changes is still working its way through the economy, but dwelling prices have firmed a little and business credit has picked up this year. The exchange rate has declined over the past month or two, though it has remained higher than might have been expected, given the observed decline in export prices and the weaker global outlook."

AUSTRALIA: From The RBA: "Growth in China remained reasonably robust in the first half of this year, albeit well below the exceptional pace seen in recent years. Some recent indicators have been weaker, which has added to uncertainty about near-term growth. Around Asia generally, growth is being dampened by the more moderate Chinese expansion and the weakness in Europe."

EU MORNING CALL - 04/09/12 The Reserve Bank of Australia held their Cash Target Rate at 3.50%, commenting that indicators suggest growth is close to trend, with inflation to stay within target for the next 1-2 years. The board said their current policy remains appropriate as previous rate cuts continue to work their way through the economy. The bank added that there is no difficulty for Australian banks to access funding, and said terms of trade for the country remain historically high.

UK BRC Like-For-Like Retail Sales (Aug) Y/Y -0.4% (Prev. 0.1%) The London 2012 Olympics failed to boost British retail sales as hoped last month, as households preferred to watch the games rather than increase consumption and spending, giving stores one of their worst months of 2012, according to the British Retail Consortium.

The Spanish finance minister De Guindos has said his country will need clear conditions before any aid application, and expects more clarity in the coming weeks. On the ESM, De Guindos said there is no doubt it will come into action in the coming months.

CIekawe że Brytyjczycy tak narzekają na olimpiadę, a u nas w kraju, gdzie każdy ma swoje zdanie, nikt nie narzeka na Euro, wręcz przeciwnie od strony ekonomicznej same zachwyty. Ale wiadomo jest druga strona medalu - stadiony i koszt ich utrzmania. Nieadwno na narodowym była impreza " Święto Ochotniczej Straży Pożarnej" Waldi "Kamienna Twarz" załatwił lokal. Mam nadzieję, że przynajmniej koszty się zwróciły w końcu to stadion narodowy, czyli Nasz

Ostatnio zmieniony 04 wrz 2012, 08:35 przez _/_/Dariusz_/_/, łącznie zmieniany 1 raz.